Is Gap Insurance Worth It on a Used Car

Gap insurance can be valuable for a used car if its loan amount exceeds its depreciation-adjusted value. It provides financial protection during the early years of ownership when depreciation is most rapid.

Gap insurance, a form of protection plan for vehicle owners, covers the difference between a car’s actual cash value and the balance still owed on financing. Is it worth considering for a used car? Absolutely, especially if you’ve taken out a significant loan to purchase the vehicle.

This insurance is particularly important in the event of total loss or theft, where standard insurance policies may fall short of covering your financial obligations. Opting for gap insurance gives peace of mind to those who invest in a used car with high depreciation rates or have a long-term loan, as it can save them from potential out-of-pocket expenses. As you weigh the pros and cons of this coverage, remember that used cars depreciate quickly, making gap insurance a smart choice for many buyers.

Gap Insurance Basics

Understanding Gap Insurance helps protect your wallet when your car is worth less than what you owe. Especially for used cars, it can be a gamechanger. Let’s dive into the essentials of Gap Insurance.

What Is Gap Insurance?

What Is Gap Insurance?

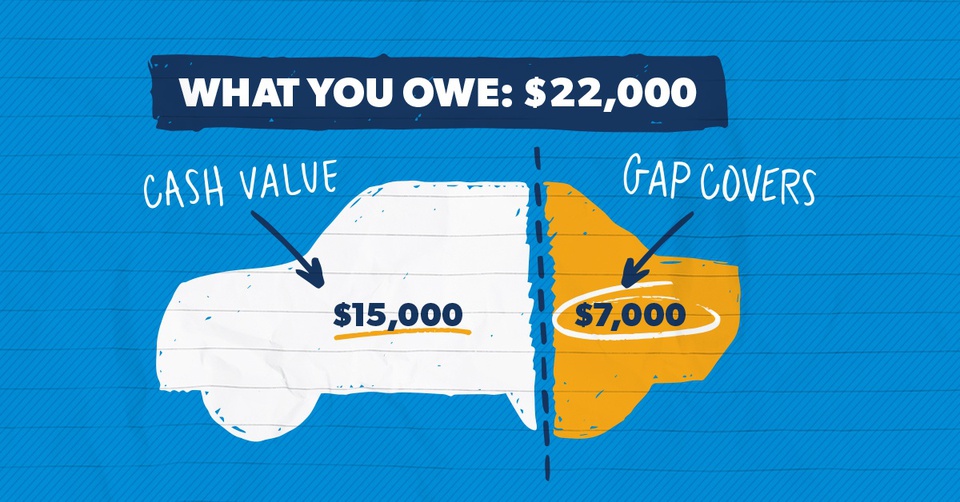

Gap Insurance, or Guaranteed Asset Protection Insurance, covers the gap between the actual value of a car and the balance still owed on it. This type of insurance is crucial if your car gets stolen or totaled and you owe more on your car loan than its current worth.

How Gap Insurance Works

When you face a total loss, Gap Insurance steps in after your standard auto insurance payout. If your standard insurance pays out less than your loan balance, Gap Insurance covers the difference. Think of it as a safety net for your car’s value and your finances.

- Claim filed with auto insurer

- Insurer pays car’s current value

- Gap Insurance pays difference if negative equity exists

Credit: privateauto.com

Depreciation And Used Cars

Understanding how a car loses value is key when looking at gap insurance for a used car. Let’s explore how quickly a car can depreciate and what that means for you.

The Moment Of Purchase

Buying a used car is the first step in a financial journey. The car’s value drops the moment it leaves the lot. This decline is an important factor in deciding on gap insurance.

Rate Of Depreciation Over Time

Cars lose value over time. The rate of depreciation differs based on the make, model, and condition. Here’s what you need to know about depreciation rates:

- New cars: Lose most value in the first year.

- Used cars: Depreciate more slowly after initial drop.

- Brand popularity: Affects how fast a car depreciates.

Maintaining a car well can slow depreciation. Gap insurance may be worth considering if depreciation outpaces your loan balance reduction.

Evaluating Your Need For Gap Insurance

Purchasing a used car often involves a significant financial commitment. Gap insurance could be a safety net that catches you if your car’s value plunges faster than your loan balance shrinks. Let’s explore when this coverage is crucial.

Loan-to-value Ratio Considerations

Understand your car’s current worth versus your loan balance. This loan-to-value ratio (LTV) is critical. If your LTV is high, gap insurance merits consideration.

- High LTV>100%: Your loan exceeds the car’s value. Gap insurance is advisable.

- LTV<100%: You owe less than the car’s worth. Gap insurance may not be necessary.

Assessing Financial Risk

Your personal financial situation dictates your need for gap insurance. Are you ready to cover the difference if your car is a total loss? Here’s why assessing your financial risk matters:

| Risk Level | Gap Insurance |

|---|---|

| Low risk | Spare funds to cover the gap mean you might skip it. |

| High risk | Limited savings suggest gap insurance could be a lifesaver. |

A tight budget with little room for unforeseen expenses heightens the importance of gap insurance. Assess these factors diligently to make an informed decision.

Pros And Cons Of Gap Insurance For Used Cars

Thinking about getting gap insurance for your used car? It’s essential to weigh the pros and cons.

Potential Benefits

Gap insurance covers the difference between what you owe on a car loan and the car’s value if totaled or stolen.

- Financial Protection: Guards against owing more than the car’s worth.

- Paid-off Loan: Ensures loan repayment after total loss or theft.

- Peace of Mind: Offers comfort knowing you’re covered.

Drawbacks To Consider

However, this insurance might not be perfect for everyone.

- Additional Cost: Increases monthly expenses with insurance premiums.

- Depreciation: Most beneficial shortly after purchase due to rapid value loss.

- Coverage Limits: May not cover unrelated costs like extended warranties.

Alternatives To Gap Insurance

Exploring alternatives to gap insurance for a used car is essential. Knowing options can save money. Let’s examine suitable alternatives.

Traditional Insurance Options

Standard car insurance may cover needs without gap insurance. Comprehensive and collision coverage are key. They pay for car damage from accidents, theft, or natural disasters. Liability insurance is mandatory in most states. It covers others’ property damage and medical expenses from accidents you cause.

- Comprehensive Coverage: Protects against non-collision-related events.

- Collision Coverage: Pays to repair your car after a crash.

- Liability Insurance: Covers others’ costs in accidents you’re responsible for.

Saving Instead Of Spending On Gap

Building a savings buffer could be smarter than buying gap insurance. Save the amount you’d pay for gap insurance. Use it for car-related emergencies or if a car’s value drops suddenly. Unlike gap insurance, savings can cover various emergencies.

- Calculate potential gap insurance costs.

- Set aside funds regularly in a savings account.

- Grow a financial cushion to handle unexpected car value drops.

Making The Decision

Making the right choice on gap insurance for a used car relies on understanding its value in relation to your specific situation. Each driver’s needs differ, so let’s explore when this type of coverage is beneficial and when it might not be necessary.

When Gap Insurance Makes Sense

Gap insurance provides financial protection in cases where your car’s value drops faster than the loan balance decreases. Here are a few scenarios where purchasing gap insurance for a used car is highly recommended:

- High-Debt Financing: If you finance a used car and your loan amount exceeds the car’s value, gap insurance can save you from potential losses.

- Small Down Payment: A down payment below 20% might lead to owing more than the car’s worth at some point.

- Long-Term Loan: Loans exceeding five years can increase the duration of negative equity, where gap insurance comes in handy.

Situations To Skip Gap Insurance

Although gap insurance is beneficial in many circumstances, there are times when it may not be a wise investment. Consider skipping gap insurance if the following situations apply:

- Significant Down Payment: If you put down a large amount up front, you’re less likely to owe more than the car’s worth.

- Quick Loan Repayment: Planning to pay off the car quickly reduces the risk of negative equity.

- Low Depreciation Vehicle: Some used cars hold their value well, diminishing the need for gap insurance.

Credit: nkyinsurance.com

Frequently Asked Questions For Is Gap Insurance Worth It On A Used Car

What Is Gap Insurance On Cars?

Gap insurance covers the ‘gap’ between what your car is worth and what you owe on it. It’s essential if your car’s depreciation outstrips your loan balance, meaning you owe more than its current value.

Does Gap Insurance Make Sense For Used Vehicles?

Yes, gap insurance can be beneficial for used cars if you have a high loan amount relative to the car’s value. It’s particularly useful if the vehicle depreciates rapidly, posing a risk of being underwater on your loan.

How Does Depreciation Affect Gap Insurance Need?

Depreciation can create a situation where you owe more than your car’s market value. Gap insurance is designed to cover this difference in case of total loss or theft.

What’s The Cost Of Gap Insurance For Used Cars?

The cost of gap insurance for used cars varies but generally ranges from $20 to $40 a year when added to comprehensive and collision coverage. Prices may vary based on provider and vehicle value.

Conclusion

Navigating the decision to invest in gap insurance for a used car hinges on personal financial protection. Evaluating the vehicle’s value against loan balance is crucial. For peace of mind and safeguarding against unforeseen losses, consider the coverage’s merits. Ultimately, gap insurance can be a prudent choice, contingent on your particular circumstances and the investment in your automotive asset.